In today’s intricate service economy, your professional advice, designs, or consultation is your greatest asset and, simultaneously, your greatest potential liability. Every recommendation you make and every service you deliver carries an inherent risk of human error, miscommunication, or unforeseen omission. While you strive for perfection, a single mistake can lead to significant financial loss for a client, potentially resulting in a devastating lawsuit against your firm. This is where Professional Indemnity insurance (PI), also known as errors and omissions insurance, becomes not just a safety net, but a fundamental component of your business strategy. This comprehensive guide from AMGib will walk you through precisely what PI insurance is, why it is critical for sustaining growth, and how the right policy provides the robust legal and financial backing necessary to protect your business's future and reputation.

What is Professional Indemnity (PI) Insurance?

Professional Indemnity insurance is a specialised form of liability coverage designed to protect service-based businesses and professionals against claims of financial loss arising from the provision of your services. Specifically, it covers claims made by clients alleging that they suffered financial harm due to an error, omission, or act of negligence in the professional service or advice you provided.

Unlike general liability insurance, which covers physical damage or bodily injury, PI insurance focuses on 'pure economic loss.' It is the essential protection for businesses where their primary value lies in their intellectual output, expertise, and advice. In essence, it serves to indemnify the professional against the costs of defending a claim and any damages or settlements that may be awarded to the client, thereby safeguarding the company's balance sheet.

Why PI Insurance is a Pillar of Business Strategy

For any business offering professional services, having adequate professional liability coverage is not a luxury, it's a non-negotiable strategic necessity. It underpins stability, facilitates growth, and provides peace of mind that allows you to focus on client delivery.

Financial Protection

The cost of defending a professional negligence lawsuit, even one that is ultimately dismissed, can be astronomical. PI insurance provides a crucial layer of financial defense, covering legal defense costs such as solicitor fees, court costs, and expert witness expenses. If the claim is successful, the policy covers the settlement or compensation awarded to the client, up to the policy limit. Without this protection, a single, significant claim could easily bankrupt an otherwise thriving small or medium-sized enterprise. This is the ultimate form of risk management for services.

Reputation Protection

A lawsuit, regardless of its merit, can severely damage a business's standing in the market. By having a robust PI policy, you can:

- Respond swiftly: Access to legal experts allows you to address the claim professionally and promptly, mitigating public relations damage.

- Demonstrate responsibility: By having the means to fully compensate a client for a proven error, you demonstrate a strong duty of care and commitment to professional standards, helping to restore trust.

Client Confidence & Contractual Compliance

Many major clients, particularly those in the government, finance, or large corporate sectors, will not engage a consultant or service provider who lacks appropriate PI cover. The policy acts as a quality assurance marker.

Furthermore, it is increasingly common for contracts to stipulate a minimum level of indemnity as a contractual requirement before work can commence. For many professions, such as independent financial advisors and solicitors, it is a mandatory regulatory requirement.

Who Needs This Essential Coverage?

Anyone who provides professional advice, design services, or intellectual work may face claims if a client experiences financial loss due to an error or omission. Professional Indemnity Insurance is essential for:

- Consulting & Management

Examples: Management Consultants, Business Analysts, HR Consultants

Key Exposure: Inaccurate advice leading to operational or strategic failures. - Technology & IT

Examples: Web Developers, IT Consultants, Software Engineers

Key Exposure: System failures, data breaches, or coding errors that disrupt client operations. - Creative & Media

Examples: Marketing Agencies, Graphic Designers, Advertising Consultants

Key Exposure: Copyright issues, misuse of creative assets, or campaigns that fail to meet agreed objectives. - Design & Technical

Examples: Architects, Engineers, Surveyors, Quantity Surveyors

Key Exposure: Design flaws or technical miscalculations resulting in construction problems or project delays. - Finance & Accountancy

Examples: Accountants, Bookkeepers, Tax Advisors

Key Exposure: Miscalculations, incorrect tax filings, or errors in auditing. - Healthcare & Law

Examples: Solicitors, Barristers, Therapists

Key Exposure: Incorrect legal advice, misdiagnosis, or treatment-related errors.

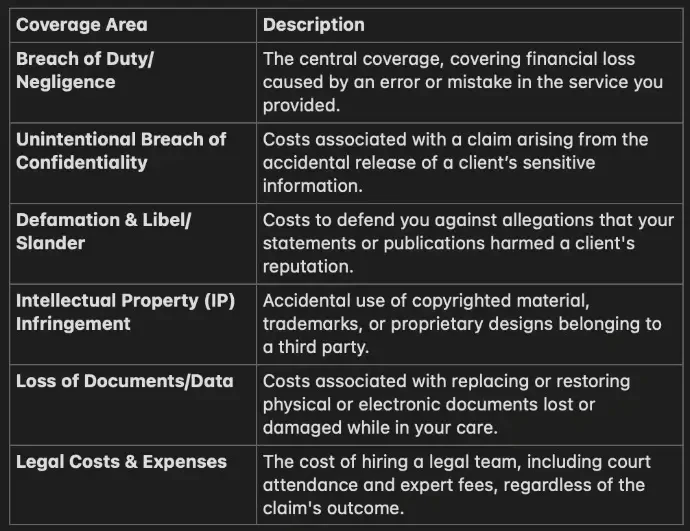

A Practical Look at What Your PI Policy Covers

Your PI policy is designed to respond to claims of civil liability arising from a breach of your professional duty. While policies vary, a typical comprehensive policy from AMGib will generally cover:

Professional Indemnity insurance is almost always written on a claims-made policy basis. This means the policy must be active both when the alleged error occurred AND when the claim is reported to the insurer. This makes maintaining continuous cover essential, even after you stop trading "run-off cover"

A Practical Look at What Your PI Policy Covers

At AMGib, we understand that a web developer's risks are fundamentally different from those of an architect. This is why we don't offer generic, off-the-shelf policies.

Our approach is built on a deep consultation process, where we meticulously assess your specific operational risks, contractual liabilities, and regulatory requirements. Our specialists have years of experience structuring policies for complex service industries, providing you with a truly bespoke solution that offers maximum protection without over-insuring.

When you partner with AMGib, you gain:

- Industry Expertise: Access to underwriters who specialise in your professional field.

- Comprehensive Coverage: Policies that address the full spectrum of your consultant liability.

- Dedicated Claims Support: Fast, expert handling of any claim to ensure minimal disruption to your business.

Let AMGib be the strategic partner that secures your professional success.

Frequently Asked Questions (FAQs)

What is the difference between Professional Indemnity and Public Liability insurance?

Public Liability (PL) insurance covers claims for bodily injury to third parties or damage to their property arising from your business activities (e.g., a client tripping over a cable in your office). Professional Indemnity insurance (PI), in contrast, covers financial loss to a client resulting from a failure in your professional service, advice, or design. They are complementary policies, and most businesses require both.

How much cover do I need?

The appropriate level of cover depends on several factors: the potential magnitude of financial loss your advice could cause a client, the maximum limit required by your regulatory body, and the minimum amount stipulated in your client contracts. We recommend reviewing your largest potential contract values and discussing them with an AMGib advisor to determine a safe and compliant level.

What is a "retroactive date" and why is it important?

A retroactive date is a feature of a claims-made policy that limits the policy’s coverage to claims arising from work performed after that specified date. It is essential because it prevents you from being covered for work you completed before you first purchased the policy. To ensure continuous coverage for all past work, your current policy's retroactive date should be the day you first began continuous professional work.

Does PI insurance cover work done by my subcontractors?

Generally, yes, if the subcontractor is working under your direct instruction and the claim is brought against your firm for work performed as part of your overall contract with the client. However, you must carefully review the policy wording. For complex arrangements, AMGib can structure your policy to explicitly include subcontractors, though you should still ensure all subcontractors carry their own adequate PI coverage.