In today's complex supply chain risk environment, virtually every business that designs, manufactures, distributes, or sells a physical product faces the inherent risk of a devastating lawsuit. A simple flaw, a manufacturing defect, a poor design defect, or inadequate warning (failure to warn) can lead to property damage, financial loss, or, most critically, severe consumer harm. This is where Product liability insurance (often shortened to PI insurance) becomes an indispensable shield. At AMGib, we understand that a single, unforeseen consumer injury claim can threaten the viability of an otherwise successful enterprise. This guide will walk you through the necessity of this coverage, the types of claims you might face, and how AMGib can provide tailored, robust protection to safeguard your assets and reputation.

What is Product Liability Insurance (PI insurance) ?

Product liability insurance is a specialized form of business liability protection designed to cover the legal defense costs and damages resulting from claims that a product you sold, manufactured, or distributed caused bodily injury or property damage to a third party.

Unlike a standard commercial general liability (CGL) policy, which primarily covers risks on your premises or from your operations (e.g., a slip-and-fall accident), PI insurance specifically targets the risks associated with the product itself once it has left your control. Essentially, if your product is alleged to be the cause of harm, this policy steps in. Think of it as defective products insurance. It's the financial backbone that allows your business to withstand an expensive and time-consuming lawsuit without draining your operational capital.

The Three Core Types of Product Liability Claims

Product liability lawsuits generally fall into three distinct categories, all of which are typically covered under a comprehensive product liability insurance policy:

1.Manufacturing Defect: This occurs when a product is manufactured incorrectly, deviating from its intended design. The design itself is safe, but an error in the assembly or production process makes a specific unit or batch dangerous.

Example: A batch of children's toys contains small, unsecured screws due to a machine malfunction on the assembly line, posing a choking hazard.

2.Design Defect: This claim asserts that the product's fundamental design is inherently dangerous, regardless of how perfectly it was manufactured. The product is marketed as intended, but its design makes it unsafe for its foreseeable use.

Example: A machine is designed without an adequate safety guard around a moving part, which could easily injure a user's hand during normal operation.

3.Failure to Warn (Marketing Defect): These claims allege that the manufacturer failed to provide adequate warnings or instructions about non-obvious dangers associated with the product's use. The product might be safely designed and manufactured, but the lack of clear labeling or instructions makes it dangerous.

Example: A medication does not clearly warn consumers about a serious side effect that occurs when mixed with a common over-the-counter drug. This falls under the critical area of failure to warn.

Which Businesses Need This Essential Protection?

The name "Product Liability Insurance" often misleads businesses into thinking only manufacturers need it. In reality, the liability net is cast much wider. If you play any role in bringing a product to the end-user, you have exposure:

- Manufacturers: You have the highest exposure, responsible for design, production, and quality control.

- Wholesalers & Distributors: Even if you don't make the product, you are often included in a lawsuit as the next point in the supply chain risk. You are legally a crucial link in the chain of commerce.

- Retailers & E-commerce Sellers: If you put your private label on a product or are the only entity the consumer can easily identify, you are highly likely to be sued alongside the manufacturer.

- Importers: Bringing products from overseas introduces complex jurisdictional issues and requires robust quality control insurance to cover foreign-made goods.

If your business liability profile includes a physical product, this insurance is not optional; it's a fundamental requirement for sound risk management for products.

Understanding Your Coverage: What a Policy Includes (and Excludes)

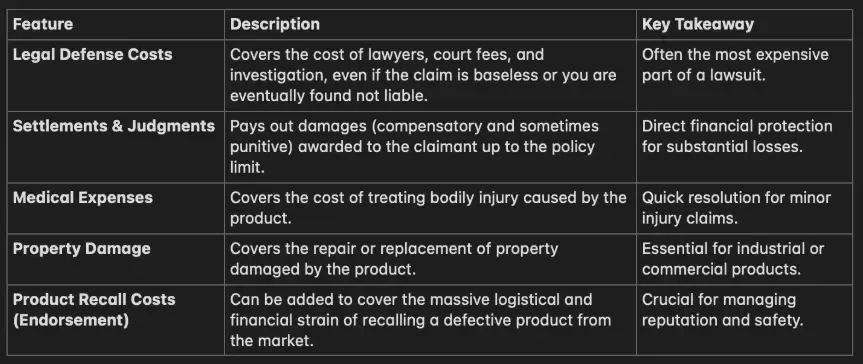

A robust PI insurance policy is tailored to your specific product and industry. Here is a general breakdown of what you can expect:

Coverage Overview:

Common Exclusions:

It is equally important to understand what product liability insurance typically excludes:

- Breach of Contract: Claims related to a product failing to meet performance specifications (this is usually covered by E&O or warranty).

- Employee Injuries: Covered under Workers' Compensation insurance.

- Intentional Harm: Damages resulting from intentionally harmful acts.

- Damage to Your Own Product: The cost of repairing or replacing the defective product itself.

The AMG Difference: A Proactive Approach to Product Risk

At AMGib, we don't just sell defective products insurance; we partner with you on risk management for products.

- Deep Industry Expertise: Our team specializes in complex product lines, from advanced electronics to food and beverage. We understand the specific supply chain risk inherent in your sector

- Tailored Policy Structure: We help you determine the optimal limits, sub-limits, and endorsements (like product recall costs coverage) based on your global sales, distribution channels, and the inherent risk of your product.

- Claims-Made vs. Occurrence: We guide you through the critical distinction between an occurrence policy (which covers incidents that occurred during the policy period) and a claims-made policy (which only covers claims that are filed during the policy period). Most PI policies are written on a claims-made basis, and understanding the implications of retro-dates is vital for continuous coverage.

- Integration with CGL: We ensure your PI insurance works seamlessly with your existing commercial general liability policy, eliminating coverage gaps and ensuring that all potential exposures are covered under your broader business liability umbrella. We help you secure robust quality control insurance that minimizes the chance of a claim in the first place.

Choosing AMGib means securing a policy that is not just compliant, but comprehensive and crisis-ready.

Frequently Asked Questions (FAQs)

Isn't product liability covered under my General Liability policy?

While some basic commercial general liability (CGL) policies may offer a minimal amount of coverage for bodily injury or property damage caused by a product, this coverage is often insufficient, capped at lower limits, or contains restrictive endorsements. A dedicated Product liability insurance policy provides the specific, high-limit protection necessary for expensive product lawsuits and manages complex risk management for products that a standard CGL policy is not designed to handle.

Am I liable if I only sell a product made by someone else?

Yes, you are. Under the legal principle of "stream of commerce," anyone in the distribution chain manufacturer, wholesaler, distributor, retailer can be named in a consumer injury claim. If you are the retailer, the injured consumer will often sue you because you are the most direct point of contact. This is why all resellers need PI insurance, functioning as robust defective products insurance, even if the ultimate fault lies with the manufacturer.

What is a "claims-made" policy?

A claims-made policy only covers claims that are filed during the specific period the policy is in effect. This contrasts with an "occurrence" policy, which covers incidents that occurred during the policy period, regardless of when the claim is filed. Because product defects can take time to manifest, PI insurance is often written as a claims-made policy. It is essential to maintain continuous coverage and consider "tail" coverage if you switch insurers or retire to cover future claims arising from past sales.

How are premium costs for product liability insurance determined?

Premium costs are determined by several critical factors:

Product Type: The inherent risk of the product (e.g., medical devices are riskier than simple hand tools).

Sales Volume: The number of units sold or the total revenue generated.

Geographic Reach: Selling globally, particularly in the US market, increases exposure and cost.

Loss History: Your business's history of past claims.