Liability is one of the most fundamental yet often misunderstood concepts in the world of business and risk management. Whether you’re a small business owner, a manufacturer, a logistics operator, or a professional service provider, understanding liability is essential for safeguarding your operations, finances, and reputation. At its core, liability refers to a legal obligation or financial liability that arises when an individual or organization is held responsible for an act, omission, or event. These obligations can stem from contractual commitments, negligence, product defects, operational errors, or even unforeseen disruptions such as event cancellations or political violence.

Because liability can surface in countless ways, it plays a critical role on both your balance sheet and your risk management strategy. Businesses in Thailand from medical clinics to freight forwarders, port and terminal operators, warehousemen, manufacturers, and even event organizers face industry-specific exposures every day. Without the right protection, a single third-party claim, damages, or lawsuit can jeopardize your assets, cash flow, and long-term viability. This guide breaks down the essentials of liability, explains how it affects your business, and shows how you can manage and mitigate these risks strategically.

The Two Faces of Liability: Financial vs. Legal Responsibility

Liability isn’t just a legal concept, it's also a financial one. To understand it fully, we have to look at it from both perspectives.

Liability on the Balance Sheet (The Accounting View)

From an accounting standpoint, liability refers to any financial obligation a business must settle in the future. This includes accounts payable, long-term loans, accrued expenses, tax liabilities, and other commitments. These obligations appear on the balance sheet because they directly influence a company’s financial health and liquidity.

In more complex industries such as transportation, port operations, or product manufacturing liabilities can also include potential obligations tied to warranties, product recalls, or pending litigation. While not all of these liabilities are certain, they represent business risk that can impact forecasts, solvency, and investor confidence.

Liability in the Eyes of the Law (The Risk View)

Legally, liability refers to an individual’s or organization’s duty of care to avoid causing harm, loss, or injury to others. When this duty is breached often through negligence, errors, or omissions the responsible party may be required to compensate affected individuals or businesses.

This legal responsibility can manifest in many forms:

- General liability claims related to bodily injury or property damage

- Product liability for manufacturers

- Medical malpractice for healthcare providers

- Public liability for businesses with physical premises

- Carrier’s liability or freight forwarder liability for logistics companies

- Port & terminal operator liability for maritime operations

- Event cancellation liability for organizers

- Terrorism and political violence liability in high-risk environments

Because the legal environment varies across industries, specialized coverage such as general liability insurance, product liability, or industry-specific liability policies is often necessary to protect your business from unexpected claims.

Common Liability Risks Every Business Faces

Even the most well-managed business can face liability exposures. Some of the most common risks include:

- Third-party injury or property damage

Accidents on your premises, equipment malfunctions, or improper safety protocols can lead to costly claims. - Professional negligence or errors and omissions

Consultants, engineers, and service providers risk being held accountable for advice or services that cause financial loss. - Product defects

Manufacturers may be held liable for design flaws, production errors, or inadequate warnings. - Logistics and transportation risks

Carriers, warehouse operators, and freight forwarders can face claims for damaged cargo, delays, or mishandling. - Medical or professional malpractice

Healthcare professionals must manage high-stakes risks associated with clinical errors or treatment complications. - Event cancellations

Organizers may face financial consequences if unforeseen disruptions cancel or delay an event. - Political violence or terrorism incidents

Businesses operating in volatile regions risk property damage, operational shutdowns, or legal complications.

Because these exposures vary by industry, a tailored indemnity structure is essential to ensure strong asset protection.

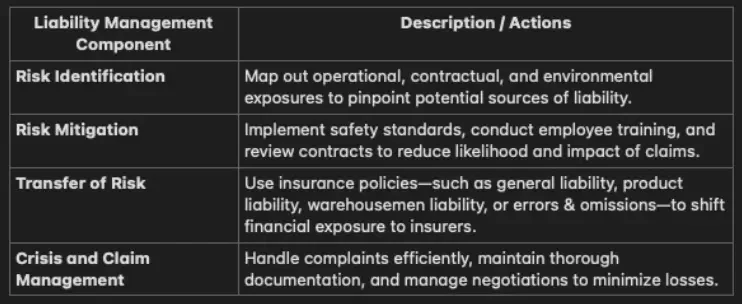

From Risk to Resolution: How Liability is Managed

Managing liability involves understanding risks, implementing preventive measures, and securing appropriate insurance. The most effective approach includes:

Summary: By integrating these steps, businesses can transform uncertain exposures into structured protection, proactively managing liability and safeguarding operations.

A Strategic Approach to Managing Your Liability Exposure

Protecting your business from liability requires a proactive and strategic mindset. Here are the key principles:

- Understand your industry’s exposure

A jeweller’s block policy won’t match the needs of a port operator. Each industry requires specialized protection. - Review contracts carefully

Many liability issues stem from contractual misunderstandings or hidden obligations. - Regularly update your insurance coverage

Business growth changes your risk profile—your coverage should evolve with it. - Document processes and maintain evidence

Strong documentation can significantly reduce disputes in the event of claims. - Prepare for worst-case scenarios

Event cancellations, political unrest, and operational failures can happen without warning.

A well-designed risk management program not only reduces exposure but also builds long-term resilience.

Frequently Asked Questions (FAQs)

What is the difference between personal and business liability?

Personal liability applies to individuals and their personal actions, while business liability refers to risks arising from commercial activities, operations, and obligations.

What happens if you are found liable but don't have insurance?

Without insurance, you must pay for damages, legal fees, and compensation out of pocket. This can threaten your assets, financial stability, and long-term operations.

What is a "limit of liability" on an insurance policy?

The limit of liability is the maximum amount the insurer will pay for a claim. Any cost beyond this limit becomes your responsibility.

Can you be held liable even if you didn't intend to cause harm?

Yes. Liability often arises from negligence or failure to meet a duty of care—not from intentional wrongdoing.